As financial services institutions accelerate their digital transformation strategies, they are moving away from centralized, self-contained data centers and shifting toward hyper-connected ecosystems. Modern banking, wealth management, and insurance platforms are built on complex webs of third-party SaaS vendors, multi-tenant cloud platforms, distributed partner APIs, and autonomous AI models.

This macro trend completely changes the definition of operational risk. When technology rewrites market operations faster than formal corporate risk policies can be updated, security can no longer be achieved by building walls around a closed network. Today, the modern identity platform is the actual network boundary. This blog explores why financial institutions must shift from old-school, point-in-time authentication checks to a model of continuous identity governance, providing security leaders with a concrete, actionable blueprint to secure human and non-human identities across their operational footprint.

When Integration Outpaces Governance

A single identity dependency can interrupt access for millions of users in minutes. In financial services when a third-party platform or modern integration fails, the disruption instantly cripples customer portals. This halts advisor and broker workflows, stalling claims operations, and challenging an institution’s control under pressure.

This deep integration creates severe concentration risk. While most institutions maintain rigid risk assessments during vendor onboarding and procurement, those static, check-the-box reviews fail once systems enter production. Resilience can no longer be evaluated at the single-firm level alone; the entire tech stack, from model providers to upstream API orchestrators, dictates an institution’s risk profile.

In an environment where access spreads dynamically across active partners, automated pipelines, and non-human systems, speed without centralized governance becomes an active business liability.

Where Identity Programs Show Strain

To move beyond high-level concepts, financial identity teams must evaluate their infrastructure against three distinct production failure modes that traditional perimeter defenses completely miss:

Production Failure Modes in IAM

| Token Persistence Without Lifecycle | Entitlement Drift Through Exceptions | Orphaned B2B Federations |

| API Keys and access tokens stay valid indefinitely across multi-tenant SaaS nodes, leaving backdoors open past contracts. | Active partners expand permissions via temporary project exceptions that are never audited or automatically revoked. | When a partner offboards a tech worker, stale down-stream trust profiles persist. |

When these operational gaps surface, the fallout compromises operational continuity, customer experience, and compliance readiness simultaneously. Accountability cannot be outsourced to a vendor. The obligation to prove evidence of control and ensure clear oversight remains strictly with the financial institution, even when the underlying technical dependency sits entirely outside its physical network perimeter.

Moving to Continuous Identity Governance

Shifting from static credentials to a model of continuous trust requires a structured operational framework. Financial identity teams can use this three-pillar blueprint to transition their architecture from perimeter validation to real-time runtime control:

1. Implement Dynamic Lifecycle Management for Non-Human Identities (NHIs)

Service accounts, bots, API clients, and automated AI workflows now process core payments, execute fraud scoring, and route claims. The industry is witnessing a clear shift toward agentic systems that do not just summarize data but actively coordinate and transact across wholesale markets. Because these systems lack a human counterpart, their access must be governed by stricter programmatic boundaries:

- Enforce Strict Ownership Mapping: Every machine identity must be cryptographically or structurally tied to an active internal line-of-business owner to maintain an evidential accountability record. Unmapped identities must trigger automatic isolation policies.

- Eliminate Standing Privileges: Transition non-human identities from permanent administrative access to time-bound, just-in-time (JIT) scoped authorization tokens.

- Automated Secret Rotation: Programmatic credentials must rotate automatically via secure vaulting systems without relying on manual IT tracking.

2. Establish a Unified Policy Fabric Across Disparate Populations

Most financial firms govern internal employees, external independent brokers, and retail customers through separate systems and conflicting policy models. This siloing creates severe security blind spots.

- Centralize Authorization Rules: While authentication (login) can happen on different platforms (such as Okta or Auth0), the authorization engine defining what that user can do must reference a unified central compliance policy.

- Context-Aware Evaluation: Move beyond validating credentials once at login. Continuously evaluate the user’s risk score, device health, data access patterns, and geographic velocity during the active session.

3. Map Identity-First Concentration Risks

Traditional business continuity plans focus on data center outages but overlook identity platform concentration risks. Shared system-wide dependencies mean that security vulnerabilities can spread much more rapidly across highly interconnected partners.

- Identify Single Points of Failure: Audit your external SaaS dependencies to find out if multiple business units rely on a single, shared third-party API or downstream authentication server.

- Build Least-Privilege Guardrails for AI Agents: As agentic AI tools are deployed to interact with core financial databases, they must operate under strict read/write boundaries that mirror the lowest-privileged human user in that specific role.

Operational Audit Checklist for Identity Teams

Bring these four specific questions to your next planning session to uncover immediate gaps in your identity surface:

- The Offboarding Test: If an external independent brokerage firm terminates an advisor today, how long does it take for their downstream access to your internal wealth management APIs to be fully revoked? Is it instantaneous, or does it depend on a weekly batch report?

- The Machine Identity Inventory: Can your team produce a real-time, accurate list of every active API key, service account, and non-human credential currently communicating with your production data environments?

- The Exception Cleanup: Do you have an automated process that scans for, flags, and automatically revokes temporary access privileges granted to third-party consultants or partner developers after a project wraps up?

- The Blast Radius Limit: If an external SaaS vendor supporting your loan processing pipeline suffers an identity breach, do your current controls prevent that attacker from pivoting laterally into your core customer databases?

Moving From Plan to Production: The BeyondID Approach

Managing a complex enterprise identity landscape across years of evolving platform deployments and organizational change requires absolute architectural consistency.

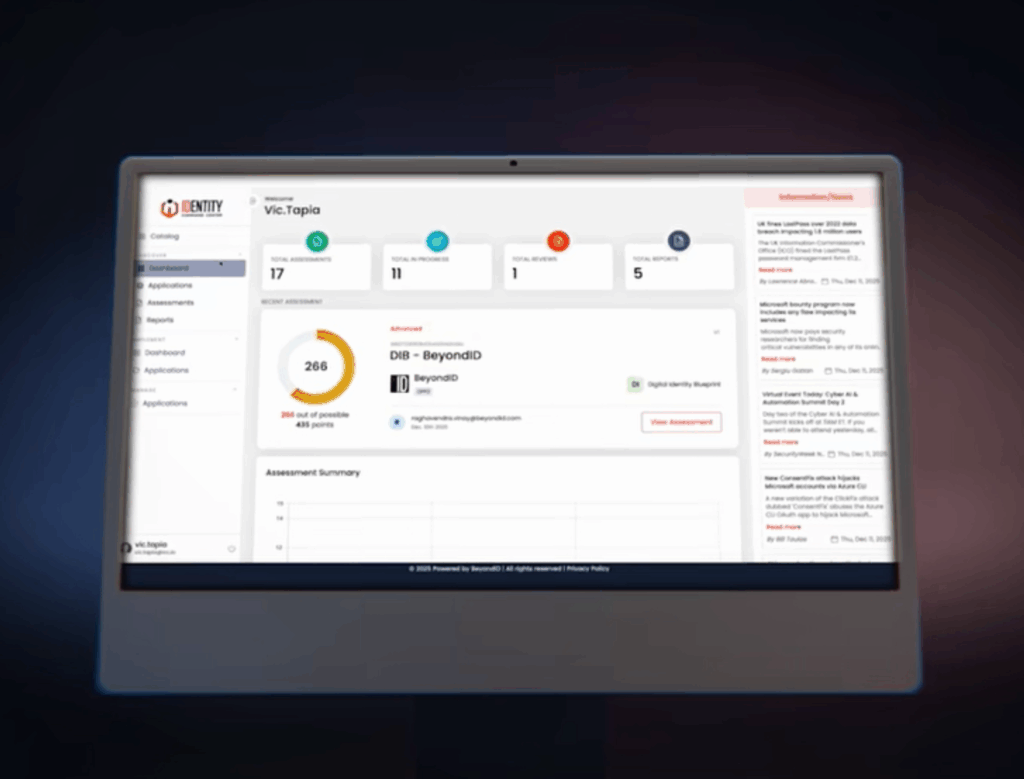

At BeyondID – a KeyData Cyber company, we help financial institutions replace fragmented projects with a unified identity-first framework. By combining our strategic Digital Identity Blueprint with the real-time risk visibility of our Identity Command Center (ICC), we translate complex engineering into measurable, boardroom-ready operational control.

Ready to evaluate the active boundary of your financial network? Connect with an enterprise architect to begin your assessment today.